SNEEK PEAK on Global Fashion Business Report 2021 | Will fashion industry rebound next year?

Author:Tom

Author:Tom

2020-10-30

2020-10-30

Key insights

- The penetration rate of online shopping in the European fashion industry rose from 16% of total sales in January to 29% in August, equivalent to a 6-year increase.

- The best estimation is that at the fourth quarter of 2020, sales in China may return to the level before the epidemic.

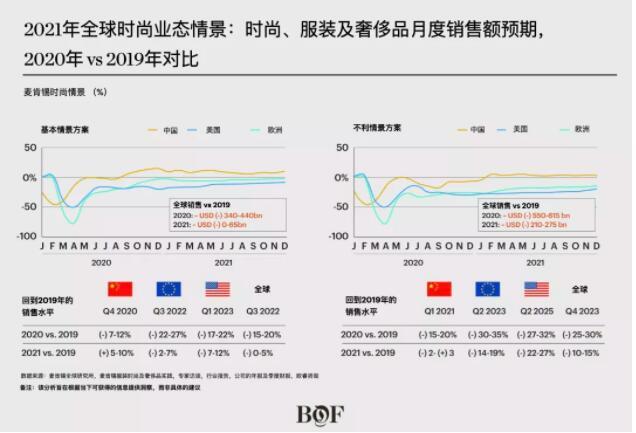

- Before the third quarter of 2022, global fashion sales are unlikely to return to the level of 2019. Any delay in mass vaccination may delay the recovery until the fourth quarter of 2023.

Sharp drop in income

This year, the global fashion industry's revenue plummeted unprecedentedly. In Europe, more than 40% of consumers decrease their spending on clothes due to general and personal economic reasons, because they feel that they do not need to buy clothes now and spend more time at home than ever before.

Now, when consumers spend money on fashion, their choices are disproportionately affected by factors such as product quality, practicality, comfort, and value for money. The importance of fashion and style begins to decline, leading people to switch to basic and casual clothing. In fact, after experiencing the inevitable deep recession at the beginning of the epidemic, sales of these categories have almost returned to their pre-crisis levels. This is in sharp contrast to formal wear and special occasion clothing. According to a recent McKinsey survey of European consumers, sales of formal wear and special occasion clothing have only recovered to 25% of last year's.

In April, May and June 2020, the total revenue of the global fashion industry fell by 34% compared to the same period in 2019. This year, the estimated loss is between $340 billion and $440 billion. An analysis of the balance sheet structure of listed companies in the European fashion industry shows that as many as three-quarters of companies may not survive without government support programs. McKinsey’s analysis predicts that assuming these subsidies will not be provided indefinitely, 20% to 30% of companies in the global fashion industry are expected to go bankrupt or be acquired by the largest and strongest companies.

This shock has already begun. Since the outbreak of the crisis, European and American fashion companies-including Neiman Marcus in the United States, J. Crew and Debenhams in the United Kingdom-have filed for bankruptcy or are using government-supported bankruptcy procedures to restructure. The total annual revenue of these companies Up to 50 billion US dollars.

Dr. Achim Berg, Global Head of McKinsey’s Fashion and Luxury Department, said: “Given that many regions of the world are currently facing a second wave of epidemics, we predict that industry turmoil will continue in 2021, and the global recovery will not show up until the second half of 2022 at the earliest. Now is the time for executives to make bold decisions and weather they are ready to get through these storms, whether it is about channel strategy, geographic focus, category planning, or ensuring supply chain security.

Map the road to recovery

The current situation may be better than what many people feared when the epidemic first broke out, but given the continued spread of the virus and the economic impact of government support measures, fashion companies need to continue to plan for a series of situations in order to make key decisions and ensure its future progress.

In the April of this year, McKinsey conducted a survey of more than 2,000 executives to find out their views on the speed and extent of the global economic recovery. Their forecast is very pessimistic, and the global GDP in the third quarter of 2020 is expected to fall by about 12% compared with the same period last year. Today’s reality is bad, but it’s not that bad—global GDP has fallen by 5%, which is a considerably optimistic result predicted by executives.

There are other signs in the past few months that help us understand how this crisis might evolve next. With the lockdown of the epidemic, online fashion sales have surged. In only 8 months, the online shopping penetration rate of the fashion industry has achieved a growth equivalent to 6 years. The proportion of online sales to total sales rose from 16% in January to 29% in August. Germany, the United Kingdom, and the five Nordic countries have largely contributed to this trend, while the digitalization process in Asia and the United States has been strong and fast. Some companies have achieved double-digit or even triple-digit growth in their online business.

Many retailers and manufacturers have proven how flexible and agile they are in expanding online channels-these qualities will be crucial in the coming years. Although the growth curve of online shopping will eventually slow down, the overall trend will continue. Among the consumers surveyed in early September, more than half said that they plan to reduce shopping in physical stores after the closure of the city, especially when the epidemic prevention measures make the shopping experience unpleasant.

But what happens when social distancing measures are relaxed and the store reopens normally? In the months following the lifting of shutdowns around the world, sales rebounded faster than expected. Consumers who have been deprived of shopping opportunities for a long time are eager to return to their favorite stores. The release of this pent-up demand means that, for some fashion retailers, sales have even returned to 2019 levels for several weeks.

In early May, China first reported this, and the same situation later appeared in Europe and North America, though it was a lesser degree. But do these early signs of recovery indicate that people's spending will quickly return to pre-crisis levels? We are still far from clear. The biggest question now is what will happen in the northern hemisphere after the summer is over.

before the third quarter of 2022, global fashion sales are unlikely to return to the level of 2019. Any delay in mass vaccination may delay this situation to the fourth quarter of 2023. But these estimates obscure the fact that at the regional and market levels, both winners and losers will exist, and the crisis has exacerbated the original trend of the industry and the obvious differences in performance between markets. What is more certain is that the recovery in various regions will be mainly driven by online sales. It is expected that offline sales will only resume after the vaccine is widely put on the market.

The Chinese market is likely to recover by the end of the fourth quarter of 2020, while Europe and the United States will take longer time.

In Europe, economic growth is likely to be equal to the global average and will not return to 2019 levels until the end of 2022. In 2020, sales during the holiday season and Black Friday will peak. During this period, sales may reach last year's level, but the overall trend is slow recovery. If the second round of shutdowns continue, the forecast will inevitably get worse, and sales this year may still fall by 30% to 35%.

Specific to the luxury goods industry, the European retail industry has been an important driving force for its growth. As tourists, especially Chinese tourists, continue to stay in the country, sales of the European luxury goods industry are expected to decline further, with a drop of 40% to 50% by the end of 2020. A similar directional decline is expected in the United States. These trends are unlikely to reverse until international travel returns to pre-epidemic levels.

In China, the situation is quite different. Luxury consumers are all spending domestically, which helps promote a faster economic recovery. According to "McKinsey Fashion Scenario Analysis Report", by the end of this year, China's luxury goods sales will increase by 8% to 13% over 2019. The main shopping season, this year's "Double Eleven" and the Spring Festival in February 2021, may see the peak of online sales. It is particularly worth mentioning that online markets such as Tmall and Taobao should perform particularly well, as retailers try to transfer excess inventory and they will benefit from increasing demand and increased supply.

In the United States, the impact of the crisis on the fashion industry was not as severe as in other regions at first, because the lockdown was later implemented and the relief checks distributed across the country supported people's consumption. However, even if the second round of the stimulus plan is expected to be launched in the fourth quarter, the long-term recovery may still lag behind China and Europe. The basic recovery time frame is not expected to appear until the first quarter of 2023. A more conservative outlook is required. It will not appear until the second quarter of 2025.

The lag in the recovery in the United States can be attributed to the low consumer sentiment that will continue to 2021. Under the basic circumstances, total fashion sales in 2020 will fall by 17% to 22% compared to 2019. Since company annual meetings, charity events, and other large gatherings are cancelled or moved online, which offset (at least minimize) the need to spend money on new clothes, we don’t expect the holiday season in the United States to be so popular like Europe’s. It is expected that the full recovery to pre-crisis levels will not be earlier than the first quarter of 2023-compared with Europe or China, this is a belated recovery.

Although there are still reasons for optimism in some sub-sectors, channels and markets of the fashion industry, overall demand will remain sluggish in 2021, and enterprise damage will inevitably occur in this process. Only those companies that make flexible decisions, respond quickly, and reflect initial consumer sentiments in their product offerings can be prepared to seize the emerging growth opportunities.

View more Chinese fashion industry report, pls visit https://www.popfashioninfo.com/analysis/market/

Shanghai Yishangyunlian Information Technology Corp. © 2004-2020Legal counsel:Beijing Zhongyin(Shanghai) Law Firms All rights reserved Shanghai ICP 06003020-19

Shanghai Yishangyunlian Information Technology Corp. © 2004-2020Legal

counsel:Beijing Zhongyin(Shanghai) Law Firms

All rights reserved Shanghai ICP 06003020-19